Insights from the AMGA 2019 Compensation and Productivity Survey

November 08, 2019

By Fred Horton, Wayne Hartley and Elizabeth Siemsen

Data from the recently released AMGA 2019 Medical Group Compensation and Productivity Survey shows a continuing trend of increases in physician compensation for many specialties without an equivalent increase in work relative value unit (wRVU) production, a trend seen in the results of last year’s survey as well. Compensation per wRVU has increased in many specialties, which poses challenges for physicians and administrators who are working to cover ever-increasing operating costs for their practices. Given these findings, one must ask how much longer compensation can continue to increase if productivity is not increasing in tandem.

Making sense of the various data points across the survey, AMGA Consulting has outlined key trends in primary and specialty care, and offered thoughts on the future trajectory of physician compensation. Given its surprising survey results this year, radiology specialties have also been given a focused analysis.

Survey participation

This year’s survey data come from 272 medical groups across the United States, representing more than 117,000 providers, including advanced practice providers (APPs). Nearly 75 percent of the survey’s compensation data comes from provider groups with more than 300 physician full-time equivalents (FTEs). Of the 272 medical group respondents, 185 identified as health system-affiliated.

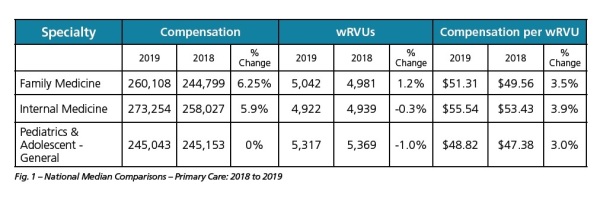

Primary care

2018 was a strong year for primary care physician compensation. Median compensation for all primary care specialties increased by 4.91 percent, which is particularly noteworthy, as last year yielded only a 0.76 percent increase. However, there was only a 0.21 percent increase in median wRVUs. As a result, the median compensation per wRVU ratio increased 3.57 percent, the largest increase in the past four years.

At the individual specialty level, family practice physician median compensation increased substantially by 6.25 percent, although it only saw a 1.23 percent increase in wRVU production. The resulting increase in median compensation per wRVU was 3.53 percent.

There are several possible reasons for the significant compensation increases primary care saw in 2018. First, AMGA members report recruitment difficulties in primary care, as a record-setting number of older physicians begin the process of retirement. Given the primary care physician shortage estimated by the Association of American Medical Colleges, it would seem there just aren’t enough physicians entering the workforce to replace those exiting it. A 2018 analysis by United Health Group shows this to be especially true in rural parts of the country.

Second, it is possible that primary care physicians have simply reached their productivity ceiling, whether due to time requirements related to electronic health records, efforts to stave off physician burnout, or the impact of increasing utilization of APPs. Nevertheless, increasing compensation with flat productivity is a concern for physicians and practice administrators.

Select specialties

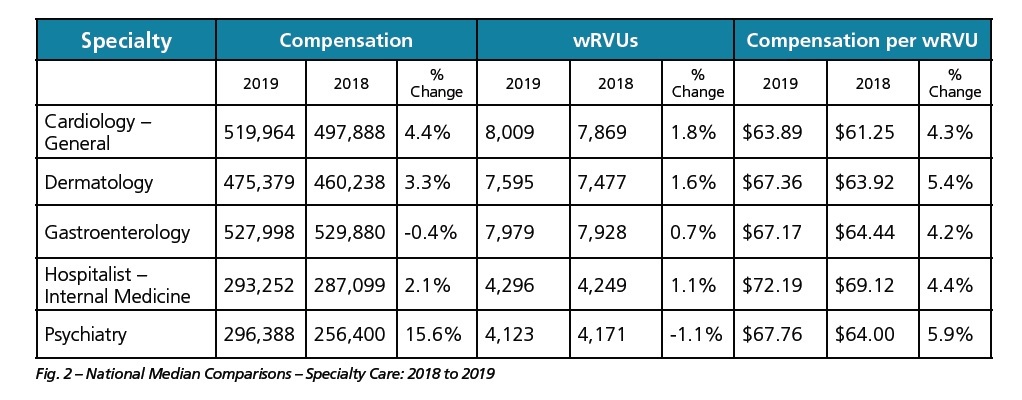

Results from our survey showed that in 2018, median compensation for all non-primary care physician specialties (excluding radiology, anesthesiology, and pathology) increased by 3.4 percent from the previous year, while median wRVU production increased by 1.9 percent. The compensation per wRVU ratio increased by 2.65 percent. A sample of medical specialties with more remarkable changes to their compensation per wRVU ratios were cardiology, dermatology, gastroenterology (GI), hospitalist–internal medicine, and psychiatry.

Of the bellwether specialties in Fig. 2, psychiatry saw the largest increase in compensation at 15.6 percent, while productivity dropped by 1.1 percent and compensation per wRVU increased by 6 percent. This compensation data is especially interesting given that psychiatrists aligned with health systems are often compensated according to a salary-based formula, as opposed to one based on production. Given the growing demand for psychiatric care and psycho-social support, this compensation increase may be a result of health systems attempting to competitively attract psychiatrists. The reduced stigma of mental health services and the recognized integration of mental health as a critical component of value-based care have encouraged organizations to optimize and stabilize their mental health workforce.

While psychiatry saw the largest jump in compensation, general cardiology saw the largest increase in wRVU production at 1.8 percent. This specialty also saw a 4.4 percent increase in compensation, and a 4.3 percent increase in compensation per wRVU. Due to a high demand for cardiology services in general and expanding clinical programs, we expect cardiologist compensation to remain strong in the future.

All five of the specialties in Fig. 2 saw compensation per wRVU increases in excess of 4 percent this past year. By comparison, many healthcare organizations are budgeting approximately 3 percent for salary increases overall. However, as we discuss next, not all specialties enjoyed a compensation increase in 2018.

Year-over-year, radiologists saw a decrease in absolute cash compensation ranging from -1.0 percent for diagnostic/non-interventional to -8.0 percent in neuro-interventional. For neuro-interventional radiology, sample size may be a factor in the data (n=103 for compensation in 2019). These programs are expanding, and in the future we anticipate a larger number of physicians will report into the survey.

Compensation decreases for radiology are even more astounding given that wRVU production increased for two of three radiology specialties — and the increases were greater than 4 percent. Given the growing reliance on capitation and bundled payments, it may be that employers and payers are devaluing individual diagnostic services in order to keep costs down without sacrificing quality.

Another possible explanation for the trends we saw may be that a clash between the health care industry’s growing emphasis on value and radiologists’ reliance on expensive imaging technology is causing a decline in median wRVU production. Value-based models simultaneously call for the delivery of preventive care and lower costs. However, in the case of comprehensive stroke programs, the need for neuro-interventional radiology presents a Catch-22. Given their somewhat limited use, neuro-interventional radiologists may not be capable of producing the volume necessary to sustain a predominantly production-based compensation model. However, to retain their vital services, it may be that health systems are opting to salary certain radiology subspecialists.

A third factor that may be affecting compensation is the way in which many radiologists choose to economically align themselves with hospitals or health systems. Radiologists often prefer to operate under an independent practice model with a service agreement between themselves and a hospital, rather than integrate with the hospital as an employee. In these affiliation agreements, physician compensation distribution may be based on something other than compensation per wRVU generated (i.e., compensation may be time- or shift-based). Regardless, decreases in overall cash compensation, especially to this extent, are likely not tolerable to radiologists so it will be interesting to observe how the market adjusts in future years.

Future trajectory

Compensation and productivity changes are not caused by any single factor. On the productivity front, concerns about physician burnout and limitations of electronic health records merit attention. The aging physician workforce and increasing prevalence of part-time physicians will accentuate recruitment and retention needs, which will exert upward pressure on compensation. Notably, the compensation values represented here are for clinical compensation and do not reflect dollars from sign-on bonuses or loan forgiveness, which are tabulated separately so as not to impact clinical compensation per wRVU metrics. Ultimately, compensation may be somewhat higher and the financial burdens for medical groups somewhat greater.

The largest unknown factor affecting compensation is the real impact of value-based care. It is possible that wRVU production has flattened because growth in utilization of services has been restricted to keep costs down. Similarly, physicians may be receiving more pay-for-performance incentives not linked directly to wRVU production. These incentives increase compensation and our calculation of compensation per wRVU in the survey data. As we work to collect future survey data in more granular detail, we hope to have more informed answers to questions around how value-based care impacts pay. In the near-term, an increased focus on practice costs and day-to-day performance will be key.

AMGA Consulting assists healthcare organizations in navigating the changing industry environment. AMGA Consulting builds clients’ organizational capabilities through effective governance, operational improvement, strategic alignment, talent management, provider compensation design, fair market value analysis and total rewards solutions. To learn more, visit www.amgaconsulting.com.

About the Authors: Fred Horton is president of AMGA Consulting. Fred has over 20 years of experience working inside the healthcare industry. He has the ability to efficiently distill complex issues and create realistic plans that lead to clients’ success. He brings his operational, strategic, and financial acumen to his clients in order to create effective and market-sensitive solutions to their challenges.

Wayne Hartley is the growth and service line development officer and VP consulting services at AMGA Consulting. He has worked in the healthcare industry for 20 years, beginning in operations and later focusing on consulting in physician services. He has spoken at national and regional conferences on FMV, physician transactions, population health, and healthcare industry trends for organizations including AHLA (American Health Lawyers Association), AMGA and HFMA (Healthcare Financial Managers Association).

Elizabeth Siemsen is a director with AMGA Consulting. Elizabeth brings more than 20 years of experience in healthcare with broad exposure to all elements of a healthcare system, including physician group practices. Most recently, she was a member of the senior leadership team of Mercy Hospital-Allina Health, and led planning and performance improvement projects for the hospital and across the system. Liz began her healthcare career as a financial analyst in decision support before expanding into performance improvement, operations and leadership roles for Allina Health and HealthEast in the Minneapolis/St. Paul area.

Data from the recently released AMGA 2019 Medical Group Compensation and Productivity Survey shows a continuing trend of increases in physician compensation for many specialties without an equivalent increase in work relative value unit (wRVU) production, a trend seen in the results of last year’s survey as well. Compensation per wRVU has increased in many specialties, which poses challenges for physicians and administrators who are working to cover ever-increasing operating costs for their practices. Given these findings, one must ask how much longer compensation can continue to increase if productivity is not increasing in tandem.

Making sense of the various data points across the survey, AMGA Consulting has outlined key trends in primary and specialty care, and offered thoughts on the future trajectory of physician compensation. Given its surprising survey results this year, radiology specialties have also been given a focused analysis.

Survey participation

This year’s survey data come from 272 medical groups across the United States, representing more than 117,000 providers, including advanced practice providers (APPs). Nearly 75 percent of the survey’s compensation data comes from provider groups with more than 300 physician full-time equivalents (FTEs). Of the 272 medical group respondents, 185 identified as health system-affiliated.

Primary care

2018 was a strong year for primary care physician compensation. Median compensation for all primary care specialties increased by 4.91 percent, which is particularly noteworthy, as last year yielded only a 0.76 percent increase. However, there was only a 0.21 percent increase in median wRVUs. As a result, the median compensation per wRVU ratio increased 3.57 percent, the largest increase in the past four years.

At the individual specialty level, family practice physician median compensation increased substantially by 6.25 percent, although it only saw a 1.23 percent increase in wRVU production. The resulting increase in median compensation per wRVU was 3.53 percent.

There are several possible reasons for the significant compensation increases primary care saw in 2018. First, AMGA members report recruitment difficulties in primary care, as a record-setting number of older physicians begin the process of retirement. Given the primary care physician shortage estimated by the Association of American Medical Colleges, it would seem there just aren’t enough physicians entering the workforce to replace those exiting it. A 2018 analysis by United Health Group shows this to be especially true in rural parts of the country.

Second, it is possible that primary care physicians have simply reached their productivity ceiling, whether due to time requirements related to electronic health records, efforts to stave off physician burnout, or the impact of increasing utilization of APPs. Nevertheless, increasing compensation with flat productivity is a concern for physicians and practice administrators.

Select specialties

Results from our survey showed that in 2018, median compensation for all non-primary care physician specialties (excluding radiology, anesthesiology, and pathology) increased by 3.4 percent from the previous year, while median wRVU production increased by 1.9 percent. The compensation per wRVU ratio increased by 2.65 percent. A sample of medical specialties with more remarkable changes to their compensation per wRVU ratios were cardiology, dermatology, gastroenterology (GI), hospitalist–internal medicine, and psychiatry.

Of the bellwether specialties in Fig. 2, psychiatry saw the largest increase in compensation at 15.6 percent, while productivity dropped by 1.1 percent and compensation per wRVU increased by 6 percent. This compensation data is especially interesting given that psychiatrists aligned with health systems are often compensated according to a salary-based formula, as opposed to one based on production. Given the growing demand for psychiatric care and psycho-social support, this compensation increase may be a result of health systems attempting to competitively attract psychiatrists. The reduced stigma of mental health services and the recognized integration of mental health as a critical component of value-based care have encouraged organizations to optimize and stabilize their mental health workforce.

While psychiatry saw the largest jump in compensation, general cardiology saw the largest increase in wRVU production at 1.8 percent. This specialty also saw a 4.4 percent increase in compensation, and a 4.3 percent increase in compensation per wRVU. Due to a high demand for cardiology services in general and expanding clinical programs, we expect cardiologist compensation to remain strong in the future.

All five of the specialties in Fig. 2 saw compensation per wRVU increases in excess of 4 percent this past year. By comparison, many healthcare organizations are budgeting approximately 3 percent for salary increases overall. However, as we discuss next, not all specialties enjoyed a compensation increase in 2018.

Year-over-year, radiologists saw a decrease in absolute cash compensation ranging from -1.0 percent for diagnostic/non-interventional to -8.0 percent in neuro-interventional. For neuro-interventional radiology, sample size may be a factor in the data (n=103 for compensation in 2019). These programs are expanding, and in the future we anticipate a larger number of physicians will report into the survey.

Compensation decreases for radiology are even more astounding given that wRVU production increased for two of three radiology specialties — and the increases were greater than 4 percent. Given the growing reliance on capitation and bundled payments, it may be that employers and payers are devaluing individual diagnostic services in order to keep costs down without sacrificing quality.

Another possible explanation for the trends we saw may be that a clash between the health care industry’s growing emphasis on value and radiologists’ reliance on expensive imaging technology is causing a decline in median wRVU production. Value-based models simultaneously call for the delivery of preventive care and lower costs. However, in the case of comprehensive stroke programs, the need for neuro-interventional radiology presents a Catch-22. Given their somewhat limited use, neuro-interventional radiologists may not be capable of producing the volume necessary to sustain a predominantly production-based compensation model. However, to retain their vital services, it may be that health systems are opting to salary certain radiology subspecialists.

A third factor that may be affecting compensation is the way in which many radiologists choose to economically align themselves with hospitals or health systems. Radiologists often prefer to operate under an independent practice model with a service agreement between themselves and a hospital, rather than integrate with the hospital as an employee. In these affiliation agreements, physician compensation distribution may be based on something other than compensation per wRVU generated (i.e., compensation may be time- or shift-based). Regardless, decreases in overall cash compensation, especially to this extent, are likely not tolerable to radiologists so it will be interesting to observe how the market adjusts in future years.

Future trajectory

Compensation and productivity changes are not caused by any single factor. On the productivity front, concerns about physician burnout and limitations of electronic health records merit attention. The aging physician workforce and increasing prevalence of part-time physicians will accentuate recruitment and retention needs, which will exert upward pressure on compensation. Notably, the compensation values represented here are for clinical compensation and do not reflect dollars from sign-on bonuses or loan forgiveness, which are tabulated separately so as not to impact clinical compensation per wRVU metrics. Ultimately, compensation may be somewhat higher and the financial burdens for medical groups somewhat greater.

The largest unknown factor affecting compensation is the real impact of value-based care. It is possible that wRVU production has flattened because growth in utilization of services has been restricted to keep costs down. Similarly, physicians may be receiving more pay-for-performance incentives not linked directly to wRVU production. These incentives increase compensation and our calculation of compensation per wRVU in the survey data. As we work to collect future survey data in more granular detail, we hope to have more informed answers to questions around how value-based care impacts pay. In the near-term, an increased focus on practice costs and day-to-day performance will be key.

AMGA Consulting assists healthcare organizations in navigating the changing industry environment. AMGA Consulting builds clients’ organizational capabilities through effective governance, operational improvement, strategic alignment, talent management, provider compensation design, fair market value analysis and total rewards solutions. To learn more, visit www.amgaconsulting.com.

About the Authors: Fred Horton is president of AMGA Consulting. Fred has over 20 years of experience working inside the healthcare industry. He has the ability to efficiently distill complex issues and create realistic plans that lead to clients’ success. He brings his operational, strategic, and financial acumen to his clients in order to create effective and market-sensitive solutions to their challenges.

Wayne Hartley is the growth and service line development officer and VP consulting services at AMGA Consulting. He has worked in the healthcare industry for 20 years, beginning in operations and later focusing on consulting in physician services. He has spoken at national and regional conferences on FMV, physician transactions, population health, and healthcare industry trends for organizations including AHLA (American Health Lawyers Association), AMGA and HFMA (Healthcare Financial Managers Association).

Elizabeth Siemsen is a director with AMGA Consulting. Elizabeth brings more than 20 years of experience in healthcare with broad exposure to all elements of a healthcare system, including physician group practices. Most recently, she was a member of the senior leadership team of Mercy Hospital-Allina Health, and led planning and performance improvement projects for the hospital and across the system. Liz began her healthcare career as a financial analyst in decision support before expanding into performance improvement, operations and leadership roles for Allina Health and HealthEast in the Minneapolis/St. Paul area.